The Central Bank of Nigeria has released a revised Guide to Charges for banks and other financial institutions, effective May 1, 2026. This updated framework replaces the 2020 version and introduces sweeping changes to how customers are charged for everyday banking services.

At its core, the policy removes fees on several routine transactions while adjusting others to reflect operational realities. As a result, millions of Nigerians will experience lower banking costs and clearer pricing structures.

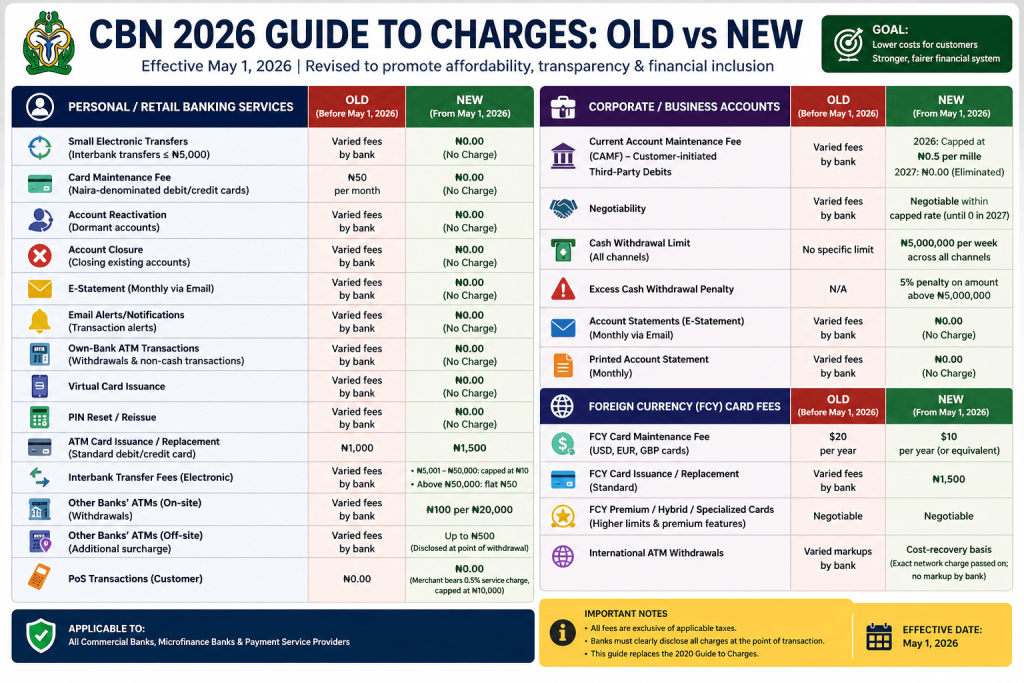

According to the new guidelines, small interbank transfers of five thousand naira and below will now attract zero fees. In addition, the monthly fifty naira card maintenance fee for naira denominated debit and credit cards has been abolished.

Furthermore, banks can no longer charge customers to reactivate dormant accounts or close existing ones. Digital banking has also been strengthened, since monthly account statements sent via email and transaction alerts must now be provided at no cost.

Customers will also benefit from free withdrawals and non cash transactions at their own bank’s ATMs. At the same time, virtual card issuance and PIN reset services will no longer attract charges.

However, not all fees were eliminated. The cost of issuing or replacing a standard debit or credit card has increased to one thousand five hundred naira. Meanwhile, interbank transfers above five thousand naira now follow a tiered structure, with a maximum of ten naira for transfers up to fifty thousand naira and a flat fifty naira fee for higher amounts.

Withdrawals from other banks’ ATMs will cost one hundred naira per twenty thousand naira. In some cases, off site ATMs may include an additional surcharge, which must be disclosed at the point of use.

Key Changes for Businesses and Corporate Accounts

The revised guide introduces notable changes for corporate banking as well. Most importantly, the current account maintenance fee will be gradually phased out.

In 2026, the fee is capped at zero point five per mille for customer initiated third party debits. By 2027, it will be completely eliminated. This phased approach gives banks time to adjust while reducing the cost burden on businesses.

Although the fee remains negotiable within the capped range, banks cannot exceed the prescribed limit. This ensures fairness while maintaining some flexibility for corporate clients.

In addition, corporate organizations now face a weekly cash withdrawal limit of five million naira across all channels. Any withdrawal beyond this threshold will attract a five percent penalty fee. This move appears designed to discourage heavy cash usage and promote digital transactions.

Monthly electronic account statements remain free, and mandatory printed statements must also be provided at no cost. These provisions strengthen transparency and ensure that businesses can track financial activity without additional expenses.

Foreign Currency Card Adjustments

The policy also addresses foreign currency cards, although changes here are more moderate. While maintenance fees for naira cards have been removed, foreign currency denominated cards will still attract charges.

That said, the annual maintenance fee has been reduced from twenty dollars to ten dollars or its equivalent. This represents a significant cut, especially for individuals and businesses that rely on international transactions.

Meanwhile, the cost of issuing or replacing a foreign currency card has been aligned with naira cards at one thousand five hundred naira. Premium and specialized cards will still have negotiable fees, depending on the bank and service features.

International ATM withdrawals will now follow a cost recovery model. Banks will pass on the exact charges from payment networks such as Visa or Mastercard without adding extra fees. This improves transparency and reduces the likelihood of hidden charges.

Why This Matters for Consumers

This policy delivers immediate and tangible benefits for everyday Nigerians. First, it reduces the cost of basic banking services, especially for low value transactions that are common among low income earners.

In addition, the removal of fees on account reactivation lowers barriers for people who may have exited the formal banking system. As a result, more individuals can return to using regulated financial services.

Digital access also improves significantly. Since email alerts and statements are now free, customers can monitor their accounts more effectively. This supports better financial decision making and reduces the risk of unnoticed charges.

Moreover, free own bank ATM transactions encourage customers to stay within their banking network, which can improve efficiency and reduce friction in everyday banking.

Implications for Banks and Financial Institutions

While consumers gain, banks will need to adapt. Fee based income has traditionally been a steady revenue stream for many financial institutions. Therefore, the removal and reduction of charges may affect short term earnings.

However, this shift could drive innovation. Banks may focus more on value added services, digital products, and customer experience to remain competitive. In the long run, stronger customer relationships could offset the loss of certain fees.

At the same time, the policy creates a more level playing field. Since all institutions must follow the same rules, competition will likely shift toward service quality rather than pricing tactics.

Read Also: New ESG Report Highlights Sustainability Challenges in Nigeria’s Banking Industry

The ESG Perspective

On the social side, the policy directly supports financial inclusion. By eliminating fees on small transactions and essential services, the framework makes banking more accessible to underserved populations. This is particularly important in a country where a significant portion of the population remains unbanked or underbanked.

In addition, improved access to free account information enhances financial literacy and empowerment. Customers can make better decisions when they have clear and timely data about their finances.

On the governance side, the policy strengthens transparency and accountability. Standardized fees reduce ambiguity, while mandatory disclosure of charges ensures that customers understand what they are paying for.

Although the environmental impact is limited, the push toward digital statements may reduce paper usage over time. However, this remains a secondary benefit rather than a core outcome.

A Policy Shift Toward Responsible Banking

This revised guide reflects a broader shift in regulatory priorities. The Central Bank of Nigeria is not only focusing on financial stability but also on consumer protection and inclusive growth.

By reducing costs and increasing transparency, the policy encourages banks to operate in a more responsible and customer focused manner. While these changes are driven by regulation rather than voluntary action, they still align with key principles of responsible business conduct.

Looking Ahead

The full impact of these reforms will become clearer after implementation. In the short term, customers will likely notice reduced charges and improved access to services.

Over time, banks may introduce new products and strategies to adapt to the changing landscape. Meanwhile, regulators will need to monitor compliance and ensure that the intended benefits reach consumers.

Ultimately, this policy marks a significant step toward a more inclusive and transparent financial system in Nigeria. While it may not transform the sector overnight, it sets a strong foundation for long term progress.

Stay informed on the policies shaping responsible business in Nigeria. Follow CSR Reporters for clear, impactful insights that matter.

[give_form id="20698"]