By Rosemary Imobhio

There is a quiet revolution happening inside boardrooms, investment committees, and regulatory offices around the world. Sustainability is no longer a feel-good sideshow to financial reporting. Today, it sits at the centre of how investors assess risk. It determines how regulators measure accountability. It also influences how companies compete for capital. Yet for years, the conversation around corporate sustainability reporting has been plagued by one stubborn problem. Too many standards, too little consistency, and far too much room for companies to say whatever they like.

That problem now has a formal answer. IFRS S1, the General Requirements for Disclosure of Sustainability-related Financial Information, is a global standard. It is designed to change how companies communicate their sustainability risks and opportunities to the world. Since its introduction by the International Sustainability Standards Board (ISSB), it has quickly become a reference point for regulators, investors, and corporations seeking a credible, comparable baseline for ESG disclosures.

For Nigeria and Africa, the stakes are particularly high. Foreign investment decisions increasingly hinge on sustainability transparency. Climate risks are intensifying. Governance expectations are rising. Understanding IFRS S1, therefore, is not an academic exercise. It is a strategic imperative for any business that wants to remain competitive, trusted, and relevant in a world that increasingly rewards transparency and punishes opacity.

What Is IFRS S1?

At its core, IFRS S1 is a standard that tells companies what sustainability-related information they need to disclose, how to disclose it, and why it matters to the people reading their reports. In simple terms, it is the rulebook for general sustainability disclosures.

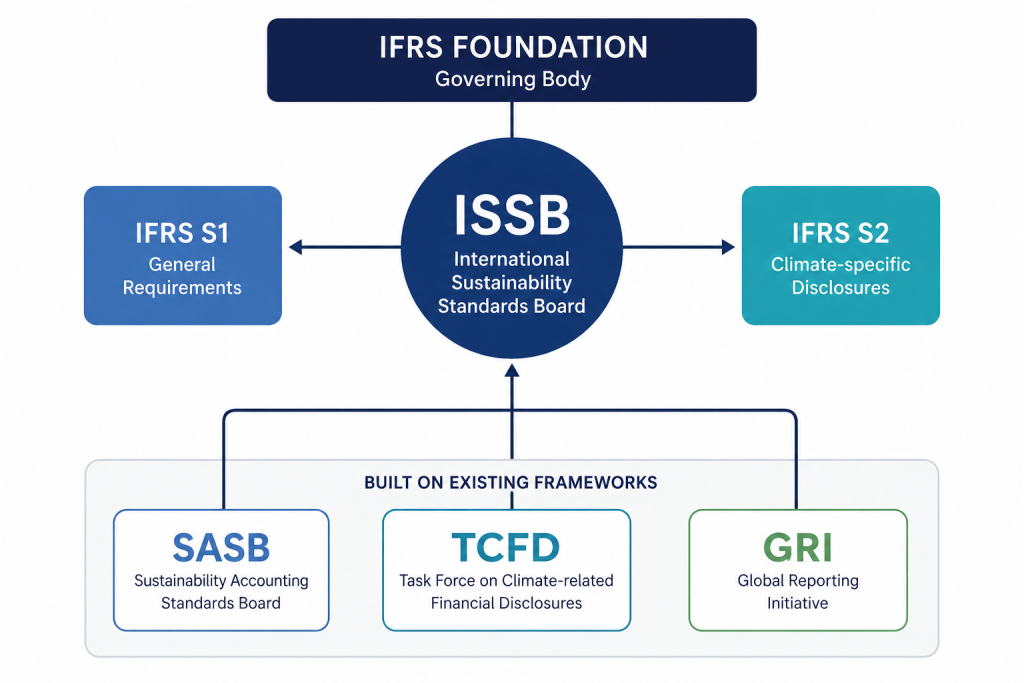

Developed by the International Sustainability Standards Board, IFRS S1 was published in June 2023 alongside its companion standard, IFRS S2, which focuses specifically on climate-related disclosures. Together, they form the IFRS Sustainability Disclosure Standards. Both standards officially came into effect on 1 January 2024.

The ISSB itself was established in 2021 under the IFRS Foundation, the same body that oversees the widely adopted International Financial Reporting Standards for accounting. The goal was clear: just as IFRS accounting standards brought consistency to how companies report their finances, the ISSB would do the same for sustainability data.

What makes IFRS S1 distinct is that it focuses on sustainability information that is relevant to investors and capital market participants. It requires companies to disclose the sustainability-related risks and opportunities that could reasonably affect their enterprise value over the short, medium, and long term. This is not about producing a glossy annual CSR report. Rather, it is about providing decision-useful information that helps investors understand what is actually at stake.

Importantly, IFRS S1 incorporates principles from the Sustainability Accounting Standards Board (SASB) standards, ensuring that industry-specific metrics remain central to how companies report. By drawing from established frameworks, IFRS S1 positions itself as a consolidating force in an otherwise fragmented sustainability reporting landscape.

Why IFRS S1 Matters for Businesses Today

Across global markets, investors are no longer satisfied with vague sustainability commitments. They want structured, comparable data. They want to understand how climate risk, governance gaps, and social pressures could affect the value of their holdings. Consequently, sustainability disclosures have shifted from a reputational exercise to a financial one.

IFRS S1 responds directly to this shift. By establishing a global baseline for what companies must disclose, it creates a common language between businesses and the investors, lenders, and insurers who depend on that information. For publicly listed companies and large corporates, alignment with IFRS S1 is increasingly becoming a prerequisite for accessing international capital markets.

Risk disclosure is another central pillar. IFRS S1 requires companies to think systematically about how sustainability-related factors, whether environmental, social, or governance-related, could affect their financial performance. This means management teams must integrate sustainability into their risk management frameworks, not treat it as an afterthought.

Furthermore, the standard drives global reporting alignment. For multinational companies operating across multiple jurisdictions, a single baseline standard reduces the burden of meeting different country-specific requirements. For investors with global portfolios, it enables meaningful comparisons that were previously impossible.

Perhaps most significantly, IFRS S1 accelerates the integration of ESG considerations into financial decision-making. When sustainability data is structured, standardised, and assured to the same rigour as financial data, it begins to inform valuations, credit ratings, and portfolio allocations in ways that scattered, voluntary disclosures never could.

| How IFRS S1 Affects Business Decision-Making |

| 📊 Investor Relations: Consistent data builds investor confidence and supports access to sustainable finance. |

| ⚠️ Risk Management: Sustainability risks must be identified and disclosed within formal governance frameworks. |

| 💰 Capital Access: Alignment with global standards signals credibility to international lenders and investors. |

| 📋 Reporting Efficiency: A single baseline standard reduces duplication across multiple reporting frameworks. |

| 🏢 Corporate Strategy: Long-term sustainability thinking becomes embedded in financial planning cycles. |

The Link Between IFRS S1 and ESG Reporting

One of the most important things IFRS S1 does is bring structure to what has historically been a chaotic ESG disclosure environment. Before its introduction, companies could choose from dozens of frameworks, report only what they liked, and present sustainability data in ways that made meaningful comparison almost impossible. IFRS S1 changes that dynamic fundamentally.

The standard anchors sustainability reporting to the concept of materiality. Specifically, it requires companies to disclose information that is material to investors, meaning information whose omission or misstatement would reasonably influence the decisions of those relying on the report. This financial materiality lens distinguishes IFRS S1 from broader stakeholder-oriented frameworks like GRI, which adopt a double materiality approach covering impacts on society and the environment as well.

On governance and accountability, IFRS S1 is equally demanding. Companies must disclose how their governance bodies oversee sustainability-related risks and opportunities. They must explain their management processes, their strategic approach, and the specific metrics and targets they use to track progress. This four-pillar structure, governance, strategy, risk management, and metrics and targets, mirrors the framework established by the Task Force on Climate-related Financial Disclosures (TCFD), ensuring continuity for companies already reporting along those lines.

Critically, IFRS S1 covers both climate and non-climate sustainability risks. While IFRS S2 handles climate in detail, IFRS S1 sets the general requirements for all sustainability-related disclosures. This means social risks, biodiversity concerns, supply chain issues, and workforce-related matters all fall within its scope where they are material to investors.

The result is a reporting ecosystem that produces genuinely decision-useful information. Investors receive structured, comparable data that helps them assess the true risk profile of a company, not a polished narrative designed to project an image.

| Before IFRS S1 | After IFRS S1 |

| Multiple, incompatible frameworks | Single global baseline standard |

| Voluntary and selective disclosure | Structured, material-based disclosure |

| Limited investor comparability | Consistent, decision-useful information |

| Narrative-led, image-focused reports | Data-driven, governance-anchored reports |

| Weak accountability mechanisms | Formal oversight and assurance pathways |

What IFRS S1 Means for Nigeria and Africa

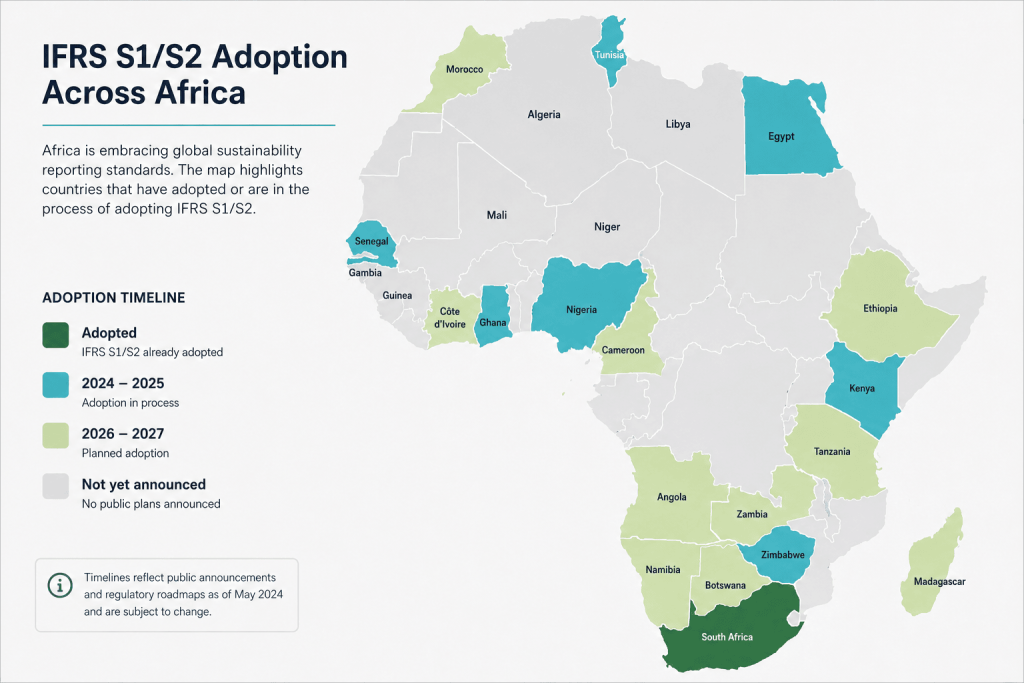

Nigeria occupies a pivotal position in Africa’s sustainability reporting journey. At COP 27 in Egypt in 2022, the Financial Reporting Council (FRC) of Nigeria became the first African country to announce its intention to early-adopt the ISSB standards. That declaration was more than symbolic. It signalled a serious commitment to aligning the country’s corporate reporting environment with global investor expectations.

In March 2024, the FRC Nigeria unveiled a comprehensive roadmap for the adoption of IFRS S1 and S2, developed through the Adoption Readiness Working Group. The roadmap set out four phases of implementation. Voluntary adoption began in the 2024 fiscal year. Large public interest entities will face mandatory compliance from 2028. Small and medium-sized enterprises are expected to follow by 2030. Then in February 2026, the FRC went further, unveiling an amended 2026 roadmap alongside the inaugural Sustainability Reporting Guideline 1 (SRG 1), which provides enhanced implementation support for Nigerian entities transitioning to the new standards.

The IFRS Foundation itself has formally recognised Nigeria’s progress. Its 2024 Progress on Corporate Climate-related Disclosures report highlighted the FRC of Nigeria for its significant contributions, listing the country among 30 jurisdictions representing 57 per cent of global GDP that are adopting or planning to implement ISSB standards.

Across the continent, adoption is gaining momentum. Kenya’s Institute of Certified Public Accountants issued a roadmap in 2024 with mandatory phased reporting beginning in 2027. Tanzania’s National Board of Accountants and Auditors adopted IFRS S1 and S2 through a Technical Pronouncement in July 2024. Ethiopia has confirmed IFRS S1 effective for reporting periods starting January 2024. The direction is clear, even if the pace varies.

For African businesses, the implications are significant. ESG-linked financing is growing. Development finance institutions, multilateral lenders, and international portfolio investors are using sustainability disclosures to screen and price investments. Companies that adopt credible, IFRS S1-aligned reporting will be better positioned to attract foreign direct investment, access green bonds, and build the kind of institutional trust that sustains long-term growth.

Challenges in Implementing IFRS S1

The ambition behind IFRS S1 is undeniable. The practical challenges, however, are equally real, and they are particularly acute in emerging markets where the infrastructure for sustainability reporting is still developing.

Data collection remains the most immediate obstacle. IFRS S1 requires companies to gather and disclose material sustainability-related information across their operations and, in many cases, across their value chains. For companies that have not previously invested in sustainability data systems, this is a significant operational challenge. Fragmented record-keeping, inconsistent measurement methodologies, and limited digital infrastructure all compound the difficulty.

The skills gap is another serious constraint. Sustainability reporting under IFRS S1 demands expertise that sits at the intersection of accounting, risk management, environmental science, and governance. Many companies across Nigeria and Africa simply do not have that expertise in-house. As noted in Nigeria’s FRC Readiness Assessment, limited technical ESG reporting skills represent one of the core frictions slowing progress toward adoption.

Cost is also a factor that cannot be ignored. Building data governance systems, training staff, engaging sustainability consultants, and eventually obtaining third-party assurance on sustainability disclosures represents a meaningful financial investment, particularly for smaller entities. The phased approach in Nigeria’s roadmap acknowledges this reality by extending the compliance timeline for SMEs.

Beyond these operational challenges, there is the risk of greenwashing. When disclosure standards are new and assurance mechanisms are still maturing, some companies may be tempted to comply in letter rather than in spirit, presenting selective or optimistic data that does not reflect the full picture. IFRS S1’s materiality requirements and the trajectory toward mandatory assurance are designed to counteract this, but the risk will persist during the transition period.

| Key Implementation Challenges |

| 📂 Data Gaps: Many companies lack structured sustainability data systems and consistent measurement tools. |

| 🎓 Skills Shortage: ESG expertise bridging accounting, risk, and environment is scarce across Africa. |

| 💸 Compliance Costs: System upgrades, training, and third-party assurance require significant investment. |

| 🔗 System Integration: Linking sustainability data to financial reporting systems is technically complex. |

| 🌿 Greenwashing Risk: Immature assurance frameworks leave room for selective or misleading disclosures. |

Can IFRS S1 Change Corporate Behaviour?

This is perhaps the most important question of all. Disclosure standards have a mixed track record when it comes to actually changing what companies do. The history of voluntary sustainability reporting is, in many ways, a history of beautiful reports that masked business-as-usual behaviour. So why should IFRS S1 be different?

Several factors suggest it will be. First, the standard is moving toward mandatory adoption in a growing number of jurisdictions. Mandatory disclosure, unlike voluntary reporting, creates legal accountability. When companies must attest to the accuracy and completeness of their sustainability disclosures, and when those disclosures are subject to third-party assurance, the incentive to be genuinely transparent increases significantly.

Second, investor pressure is intensifying in ways that directly affect corporate behaviour. As more institutional investors integrate IFRS S1-aligned data into their investment processes, companies that perform poorly on sustainability metrics face real financial consequences, whether through higher cost of capital, exclusion from ESG-focused portfolios, or reputational damage that affects their market standing.

Third, disclosure has a way of generating internal accountability. When sustainability data must be gathered, verified, and reported to investors every year, it becomes embedded in management processes. Boards start asking harder questions. Risk committees start tracking sustainability performance with the same rigour they apply to financial results. Over time, this institutional attention tends to drive genuine improvement.

Of course, none of this happens automatically. The quality of regulation, the robustness of assurance, and the sophistication of investor engagement all determine how effectively IFRS S1 translates into changed behaviour. Nevertheless, the trajectory is encouraging. Nigeria’s 2026 amended roadmap includes a formal Adoption Readiness Test requiring companies to validate their data governance and internal capacity before submitting their first sustainability report. That kind of rigour signals a shift from performative compliance to substantive accountability.

Ultimately, IFRS S1 represents a bet that transparency, consistently applied, will reshape corporate priorities over time. The evidence from other domains of financial reporting suggests that bet is well-founded. When investors can see clearly, companies that perform well on material sustainability factors tend to be rewarded, and those that do not tend to face growing pressure to change.

The Transparency Imperative

IFRS S1 is not a silver bullet. It will not, by itself, solve the complex sustainability challenges facing businesses in Nigeria, Africa, or the rest of the world. However, it does something critically important: it establishes a common language for sustainability disclosure that connects corporate performance to investor expectations, regulatory accountability, and long-term value creation.

For Nigerian businesses, the roadmap is now clear. The FRC’s phased adoption timeline gives companies the runway to build their capabilities, invest in the right systems, and develop the expertise needed to report credibly under the new standard. Those that treat this as an opportunity rather than a burden will find themselves better positioned to attract sustainable finance, build institutional credibility, and navigate the risks of an increasingly sustainability-conscious global economy.

For the wider African continent, Nigeria’s leadership in ISSB adoption sends an important signal to investors and regulators alike. Sustainability reporting standards are not a luxury of wealthy economies. They are, increasingly, the price of admission to global capital markets. IFRS S1 sets the terms. How Africa’s businesses respond will shape their economic trajectories for years to come. The era of opaque, inconsistent, and selectively curated sustainability reporting is ending. In its place, a new standard of transparency, accountability, and material disclosure is taking hold. IFRS S1 is at the centre of that transition, and understanding it is no longer optional for any business serious about its future.

[give_form id="20698"]