Nigeria’s fintech sector continues to expand at an impressive pace. Over the past few years, digital finance has moved from convenience to necessity. Today, millions of Nigerians rely on fintech platforms for payments, savings, lending, and business operations.

Companies such as Flutterwave, OPay, and Moniepoint have built strong ecosystems that support both individuals and businesses. In addition, digital banks like Kuda Bank and savings platforms like PiggyVest are reshaping how people interact with money.

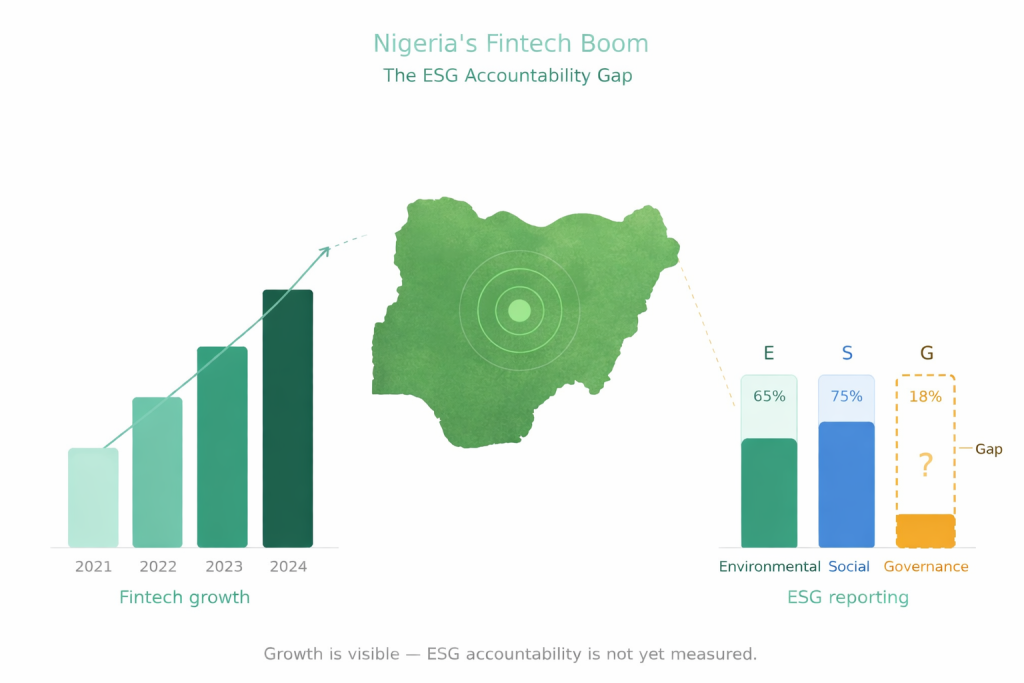

As a result, Nigeria is now widely regarded as Africa’s fintech hub. Investment activity, user growth, and product innovation continue to drive the sector forward. However, while growth is visible, another important conversation is still developing.

The Reality Check Behind the Growth

Despite this rapid expansion, structured reporting on impact remains limited. Many fintech companies highlight financial inclusion, innovation, and customer reach. However, these claims are rarely backed by standardized ESG disclosures. In other words, they discuss impact, but do not consistently measure or report it.

This gap creates an imbalance. On one hand, fintechs are solving real problems. On the other hand, there is little publicly available data to track how sustainable or responsible these solutions are over time.

Therefore, the conversation is shifting. Stakeholders are beginning to ask more direct questions about accountability, transparency, and long term impact.

Understanding ESG in Simple Terms

Environmental, Social, and Governance standards help organizations measure their broader impact. ESG does not only apply to large corporations or industrial sectors. Instead, it applies to any business that affects people, systems, and resources.

The Environmental aspect looks at energy use and digital infrastructure. The Social aspect focuses on inclusion, customer welfare, and community impact. Governance covers data protection, ethics, and transparency.

Globally, frameworks such as the Global Reporting Initiative provide guidance for companies to report these metrics in a structured way. Therefore, ESG reporting is not just about compliance. It is about building trust and demonstrating responsibility.

Fintech vs Traditional Banks: A Clear Contrast

When one compares fintech companies with traditional financial institutions, a clear difference emerges. Established banks like Access Bank and First Bank have already adopted structured sustainability reporting practices. These banks publish annual sustainability or integrated reports. They disclose environmental impact, governance structures, and social initiatives using recognized frameworks. As a result, stakeholders can assess their performance beyond financial results.

In contrast, many fintech companies have not yet adopted similar reporting standards. While some publish blog updates or impact summaries, these are often not aligned with global frameworks.

This difference does not suggest that fintechs lack impact. Instead, it highlights a reporting gap that is becoming more visible as the sector matures.

Why the ESG Gap Matters Now

The absence of structured ESG reporting carries several implications. First, trust becomes harder to measure. Customers are increasingly aware of how companies use their data and manage risk. Without transparency, confidence may weaken over time.

Second, investor expectations are changing. Global investors are placing greater emphasis on ESG performance. Therefore, fintech companies seeking long term funding may face increased scrutiny.

Third, regulation is evolving. Nigeria’s financial ecosystem is becoming more structured, particularly in areas such as data protection and consumer rights. Governance practices will play a critical role in determining which companies adapt successfully.

Finally, sustainability is not only about growth. It is about resilience. Companies that fail to track their impact may struggle to identify risks early.

Governance and Data Responsibility

Governance remains one of the most critical ESG pillars for fintech. These companies handle large volumes of sensitive financial and personal data. As digital adoption grows, the risks associated with data misuse or breaches also increase.

Nigeria has taken steps to address this through the Nigeria Data Protection Act. This law establishes clear expectations around data privacy and security.

However, compliance alone is not enough. Transparent reporting on how data is managed can strengthen public trust. It can also differentiate companies in a competitive market.

Therefore, governance is not just a regulatory requirement. It is a strategic advantage.

Financial Inclusion: Impact Without Measurement

Financial inclusion is often described as fintech’s greatest contribution. Millions of Nigerians who were previously excluded from formal banking systems can now access financial services.

Agent networks, mobile wallets, and digital lending platforms have expanded access across urban and rural areas. This progress is significant. However, the depth and sustainability of this impact are not always clear.

For example, questions remain about loan affordability, customer education, and long term financial health. Without structured reporting, these factors are difficult to evaluate.

Therefore, inclusion should not only be measured by access. It should also consider outcomes.

The Environmental Conversation Is Emerging

At first glance, fintech appears environmentally neutral. There are no factories or large scale emissions. However, digital infrastructure still has an environmental footprint.

Data centers, cloud services, and device usage consume energy. As fintech adoption grows, this footprint may also increase.

Currently, environmental reporting in the fintech sector remains limited. However, this presents an opportunity. Companies that begin tracking and disclosing environmental metrics early may gain a competitive edge.

A Turning Point for the Industry

Nigeria’s fintech sector is entering a new phase. Growth alone is no longer the only benchmark. Accountability and transparency are becoming equally important.

This shift is not unique to Nigeria. Globally, fintech companies are beginning to align with ESG expectations. Therefore, local players may need to adapt to remain competitive.

Importantly, this transition does not require immediate perfection. Instead, it begins with intentional steps toward structured reporting.

What Needs to Happen Next

First, fintech companies can begin adopting recognized reporting frameworks such as the Global Reporting Initiative. This will help standardize disclosures and improve comparability.

Second, internal systems should be developed to track impact metrics. These may include customer outcomes, data protection practices, and operational footprint.

Third, transparency should be prioritized. Even early stage reports can build credibility if they are honest and consistent.

Finally, collaboration within the ecosystem can accelerate progress. Industry groups, regulators, and media platforms all have a role to play.

From Growth to Accountability

Nigeria’s fintech sector is already transforming how money moves. However, the next phase will be defined by how impact is measured and reported. Therefore, fintech companies are encouraged to begin publishing ESG or sustainability reports. Structured reporting will not only improve transparency but also strengthen long term growth.

CSR Reporters invites fintech organizations to submit their CSR and sustainability reports for the upcoming Impact Ranking. This initiative aims to highlight accountability, not just activity.

As the sector evolves, one question will continue to shape the conversation: Can fintechs prove the impact they are creating? The answer may define the future of digital finance in Nigeria.

[give_form id="20698"]