Image credit: Ghana News Agency

Nigeria’s next-door neighbour, Ghana, has been acknowledged by experts and development partners as a regional leader in Environmental, Social and Governance (ESG) regulation in West Africa.

Speakers at a high-level ESG Roundtable for Development Partners at the World Bank Office in Accra attributed the country’s progress to steady policy reforms, coordinated institutional efforts, and strong regulatory leadership, Ghana News Agency reported at the weekend.

Speaking at the roundtable, the Environmental and Social Risk Management Specialist at the International Finance Corporation (IFC), Ms Damilola Sobo Smith, underscored the criticality of ESG for businesses, noting that companies looking to remain sustainable and competitive must now address issues such as climate change, poor waste management, labour conditions, and human rights.

In Ghana, she said, the ESG programme has helped banks to understand how environmental and social risks could directly affect business performance. For instance, challenges such as improper permits or poor waste management could lead to shutdowns and financial losses.

As a result, many banks now incorporate ESG checks into their decision-making processes, and businesses seeking loans have to meet specific environmental and social standards, which have improved transparency and accountability across sectors, she said.

Ms Smith further said regulators have increased cooperation in recent years to ensure consistent application of ESG policies across the financial system, and that has been key in positioning Ghana at the forefront of sustainable finance in the region.

Ghana’s ESG Journey

According to Ghana News Agency, the country’s ESG journey began gaining momentum in 2020 following the Bank of Ghana’s introduction of the Sustainable Banking Principles requiring banks to integrate environmental and social risks in their daily operations and lending decisions.

Since then, regulators and development partners have worked closely to strengthen the framework and ensure compliance across the financial sector, a collaboration that has gradually improved how financial institutions manage risks related to environmental protection, social responsibility, and governance.

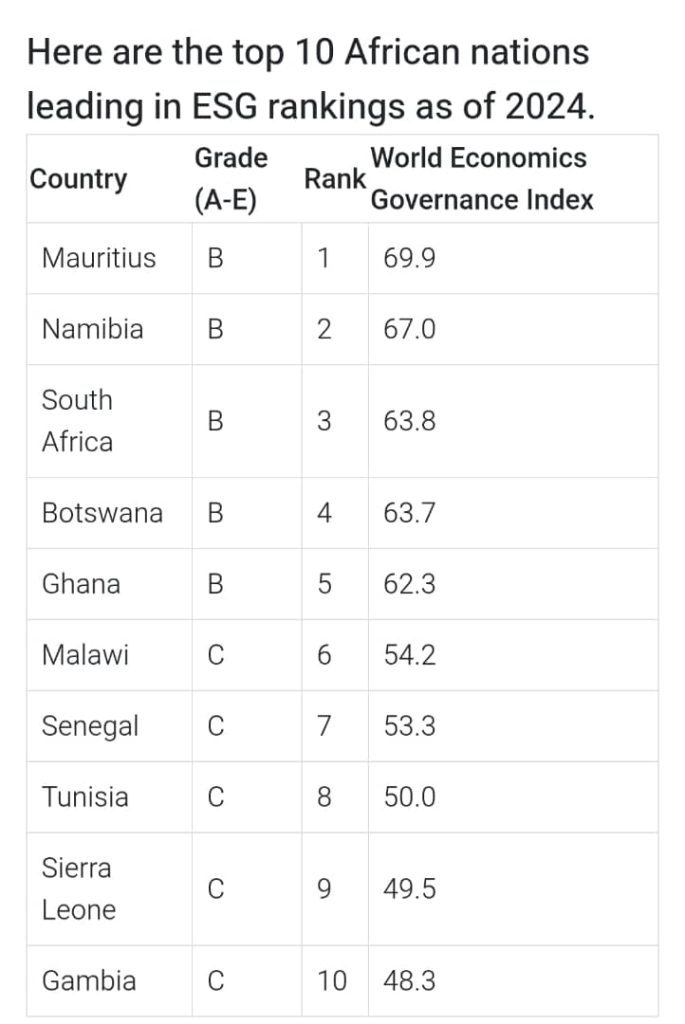

A 2024 ESG ranking, published by Business Insider Africa, placed Ghana at number 5 in Africa and number number 1 in West Africa. Mauritius led the pack, followed by Namibia, South Africa, and Botswana.

Ghana also made history in 2025 as one of the first African countries to establish a carbon market registry, issuing internationally transferred mitigation outcomes (ITMOs), and launching eco-levies on electrical equipment.

Similarly, the Ghana Stock Exchange (GSE), in a push to elevate corporate transparency and attract sustainable capital, launched the GSE’s ESG Disclosures Guidance Manual. The manual requires listed companies to adopt the Global Reporting Initiative (GRI) Standards as the common framework for ESG, according to a report by Templars titled “The Push Towards Sustainable Investments: Guidance For ESG Disclosures by Listed Companies in Ghana”.

What Ghana’s ESG Progress Means

Speaking at the roundtable, the Deputy Head of Cooperation at the Swiss Embassy in Ghana, Ms Magdalena Wüst, said the Sustainable Banking Principles have significantly strengthened Ghana’s financial sector.

She attributed the success that Ghana has made to years of institutional support and investment, saying collaboration with the IFC has helped Ghana build a resilient financial system capable of attracting investment, supporting businesses, and creating jobs.

She noted that strong ESG regulation enhances investor confidence, as investors are more likely to invest in countries with clear and reliable governance systems.

Ms. Wüst emphasised that Ghana’s achievements demonstrate the importance of effective regulation, continuous training, and strong partnerships in addressing environmental and social challenges.

Going Forward

Ghana is clearly making progress in standardising its ESG frameworks. By so doing, the country is building a highly resilient financial system that boosts international investor confidence, helps the country to avoid regulatory bottlenecks in global markets, and positions Ghanaian businesses to readily attract global climate financing and green investments.

While African countries that are lagging have a lot to learn from Ghana’s ESG progress, Ghana itself still has work to do. As the country journeys on, it must now seek ways to expand ESG implementation across all sectors of the economy to sustain progress and promote inclusive growth, as Ms Wüst suggested. Celebrating little wins is in order, but real victory comes when there is widespread corporate compliance across smaller businesses and the impact is felt in communities.

[give_form id="20698"]