By Rosemary Imobhio

Something historic happened in 2025. For the first time in over a century, renewable energy overtook coal in the global electricity mix. According to Ember Energy’s Global Electricity Review 2026 (1), renewables reached 33.8 percent of global electricity generation. Just edging past coal’s 33 percent share.

Furthermore, clean electricity grew fast enough to absorb all new global electricity demand. The result was it effectively keeping fossil fuel generation flat rather than allowing it to climb further.

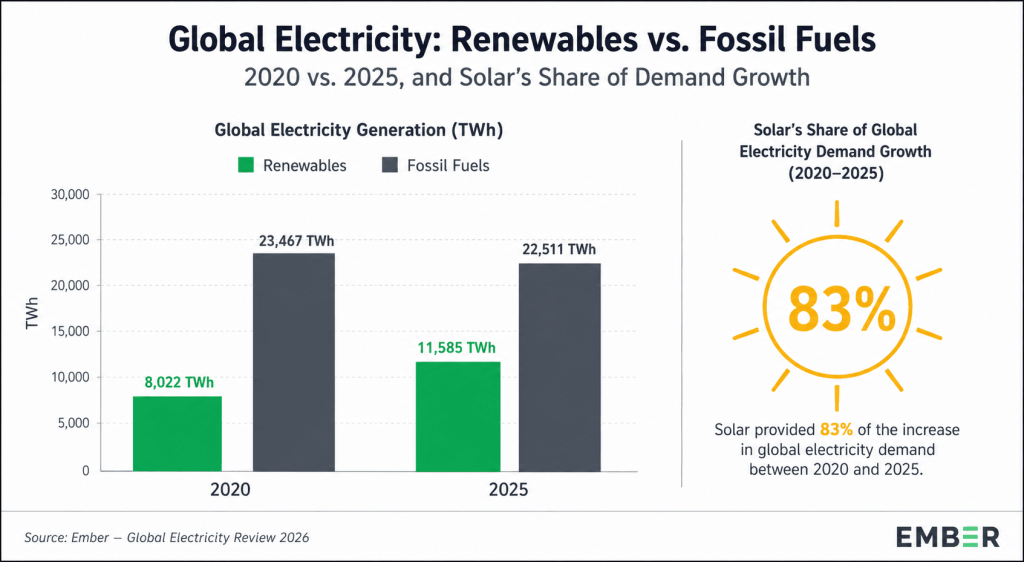

These findings, drawn from data across 215 countries, represent a genuine turning point in the global electricity transition. Solar energy alone met 75 percent of the increase in global electricity demand. While solar and wind together accounted for 99 percent of net new demand. In many respects, the numbers signal an era where renewable energy growth is no longer a policy aspiration. It is now a structural reality.

However, a closer reading of the data reveals a more complex picture. Fossil fuels remain deeply embedded in global electricity systems, and total demand continues to rise. Additionally, the transition is not happening uniformly across all regions.

For developing economies, particularly across Nigeria and the wider African continent, structural constraints, financing gaps, and infrastructure deficits mean that the global energy transition arrives unevenly. This article offers a balanced examination of what the transition means today and what it must urgently mean for Africa tomorrow.

The Global Electricity Transition in Motion

Global electricity demand grew by 849 terawatt-hours in 2025, a 2.8 percent increase compared to the previous year. Notably, low-carbon generation expanded by 887 TWh over the same period, which means that clean energy not only kept pace with rising demand but slightly exceeded it. As a result, fossil fuel generation declined marginally by 0.2 percent, and coal generation fell by 63 TWh, its first decline since the COVID-19 pandemic in 2020.

Solar power was the dominant force behind this shift. Solar generation rose by a record 636 TWh to reach 2,778 TWh in 2025, representing a 30 percent increase from the previous year. Moreover, solar capacity additions reached a record 647 GW globally.

To put that growth in perspective, solar generation has increased more than tenfold since 2015. As at then, global output stood at just 256 TWh. The technology has been roughly doubling every three years and in 2025, it overtook wind power as the world’s largest single source of new electricity generation.

Despite all of this, the transition remains structurally unfinished. While renewables are growing rapidly, total global electricity demand is also expanding. It’s driven by industrialization, electrification of transport, and the surge in data center and AI energy consumption.

Therefore, the world is not straightforwardly replacing fossil fuels. In many regions, it is simply adding renewable capacity faster than demand growth. The underlying fossil infrastructure, however, continues to operate. In that sense, the headline numbers, though genuinely historic, should be read as the beginning of a structural shift rather than its completion.

Why Fossil Fuel Dependence Remains Sticky

Even as solar energy expansion accelerates, fossil fuels continue to play a central role in electricity systems across most of the world. Understanding why is critical to understanding the pace and shape of the global electricity transition.

First, energy security concerns remain a powerful driver of fossil fuel dependence. Many governments, particularly in emerging economies, rely on domestic coal and gas reserves not only for electricity affordability but also for national economic stability. Transitioning away from these resources requires not just political will but substantial capital investment in grid modernization, storage infrastructure, and new generation capacity, all of which take years to deploy.

Second, grid limitations and storage challenges slow the integration of variable renewable energy. Solar and wind are intermittent by nature. Consequently, as their share of electricity generation rises, the need for battery storage, flexible demand systems, and upgraded transmission networks becomes increasingly urgent. Ember’s report itself noted that near-flat hydropower growth in 2025 exposed growing challenges in balancing rapidly expanding renewables on existing grids.

Third, policy inconsistency across regions undermines clean energy investment. While Europe has made sustained legislative commitments to renewable energy growth, other regions, particularly parts of Asia, Latin America, and sub-Saharan Africa, continue to face regulatory uncertainty, underdeveloped energy markets, and limited access to affordable green finance.

Finally, industrial demand adds another layer of complexity. Heavy industries such as steel, cement, and chemicals continue to depend on high-temperature fossil fuel processes that electricity alone cannot yet fully replace. As a result, even in countries with strong renewable electricity sectors, overall fossil fuel dependence at the economy-wide level remains significant.

The structural reality, therefore, is that renewable energy growth and fossil fuel dependence are currently coexisting forces in the global electricity system rather than competing ones.

The Business and ESG Reality

For corporations operating across global supply chains, the energy transition creates a dual reality: mounting pressure to decarbonize on one side and energy system inertia on the other.

ESG reporting pressure has intensified sharply in recent years. Institutional investors, rating agencies, and regulatory bodies now expect companies to disclose their energy-related emissions, set credible net-zero targets, and demonstrate active progress toward cleaner energy sourcing. Frameworks such as the Task Force on Climate-related Financial Disclosures (TCFD) and the emerging International Sustainability Standards Board (ISSB) guidelines are increasing the stakes for companies that fail to act.

In response, corporate renewable procurement has grown significantly. Power Purchase Agreements, commonly known as PPAs, are long-term contracts through which companies buy electricity directly from renewable generators. These agreements have become a mainstream tool for large multinationals seeking to lock in clean energy at competitive prices. Similarly, green tariff schemes offered by utilities in various markets allow businesses to source certified renewable electricity without owning generation assets.

Nevertheless, the clean energy investment landscape remains uneven. While large multinationals headquartered in Europe and North America have the financial capacity to access green energy markets, small and medium-sized enterprises in emerging economies often lack both the access and the capital to make similar transitions.

Furthermore, companies operating in fossil-dependent electricity markets face direct financial risk exposure. As emissions pricing mechanisms expand globally, electricity procurement from high-carbon grids may increasingly translate into higher operational costs and regulatory penalties. From an ESG and sustainability reporting perspective, the direction of travel is clear: the transition is not optional, even when the grid still runs on gas.

Nigeria and Africa in the Global Transition Gap

While the global picture is one of accelerating clean energy growth, the African story reflects a more complex and more urgent reality. According to Ember’s data, Africa’s electricity demand grew by 3.2 percent in 2025, which is above the global average of 2.8 percent. Between 2020 and 2025, clean power met only 52 percent of Africa’s new electricity demand, with the remaining 48 percent supplied by fossil fuels.

Gas remains the single largest source of electricity in Africa, accounting for 42 percent of the continent’s power generation in 2025. Gas generation across the continent rose by 44 percent between 2015 and 2025, with gas-producing countries, particularly in North Africa, increasing their reliance on the fuel.

At the same time, renewables have overtaken coal in Africa’s electricity mix for the first time, reaching 26 percent of generation. Yet despite this progress, solar energy accounted for less than 4 percent of Africa’s electricity in 2025, and the continent represented only 1.4 percent of global solar generation. This is an extraordinary underrepresentation given that Africa is the sunniest continent on Earth.

For Nigeria specifically, these continental patterns are further complicated by domestic structural challenges. Nigeria’s electricity sector has long been constrained by inadequate transmission infrastructure, gas supply inconsistencies that limit power plant output, and an electricity market that struggles to attract sufficient private investment. Millions of Nigerians, particularly in rural and peri-urban areas, remain without reliable grid access, relying instead on expensive diesel generators that contribute to both carbon emissions and economic hardship.

Read Also: Nigeria’s Energy Woes Intensify Following World Bank’s $717.7m Withdrawal

However, the transition gap also represents a genuine opportunity. Decentralized solar mini-grids and off-grid renewable systems offer a pathway to energy access that does not require waiting for centralized grid expansion. Across Nigeria and sub-Saharan Africa more broadly, community-scale solar installations are already demonstrating that affordable, clean electricity can reach underserved populations, provided that financing structures, regulatory frameworks, and public-private partnerships align to support deployment at scale.

Notably, 2025 also saw a significant increase in solar panel imports into Africa. A development that Ember analysts describe as potentially impactful for almost every country on the continent. If that early momentum translates into sustained investment, it could accelerate the uptake of cost-competitive solar across markets where energy access remains critically low.

The opportunity areas for Nigeria and Africa are substantial. These include solar mini-grids for rural electrification, off-grid renewable systems for households and small businesses, green job creation in installation and maintenance, and structured public-private partnerships that can unlock the climate finance flowing into clean energy investment globally. Africa is not behind the global transition in terms of potential. Rather, it is navigating a set of structural and financing constraints that require targeted solutions and renewed international commitment to energy equity.

Transition Is Real, but Equity Is the Unfinished Work

The global electricity transition documented in Ember Energy’s Global Electricity Review 2026 is real, measurable, and accelerating. Renewables have overtaken coal. Solar is growing at historic rates. Clean energy is now meeting all new global electricity demand. These are not incremental changes. They are structural shifts in how the world generates power.

And yet, fossil fuel dependence remains deeply embedded in global systems. Grid limitations, industrial inertia, policy inconsistency, and uneven access to clean energy investment mean that the transition is moving at very different speeds in different parts of the world. For corporations, the ESG and sustainability reporting pressure to decarbonize is intensifying regardless of where grids currently stand.

For Nigeria and Africa, the central question is no longer whether the global energy transition is happening, because it clearly is. The more pressing question is how quickly African countries can align their policy environments, infrastructure investment, and financing access to become active beneficiaries of that transition rather than passive bystanders to it.

The global shift toward clean energy offers Africa a genuine opportunity to leapfrog aging fossil infrastructure. To expand energy access through decentralized solar systems. And to build electricity sectors that are both sustainable and equitable. Realizing that opportunity will require not only domestic commitment but also a global clean energy investment architecture that takes energy equity as seriously as emissions reductions.

References

- Ember. (2026, May 21). Global Electricity Review 2026 | Ember. https://ember-energy.org/latest-insights/global-electricity-review-2026/