The numbers no longer lie quietly in spreadsheets. Across the globe, floods are disrupting supply chains, droughts are threatening food systems, and wildfires are forcing insurers out of entire regional markets. For investors, lenders, and regulators, climate change has stopped being a distant environmental concern and become a pressing financial risk. Yet, for years, the corporate world lacked a consistent, credible way to disclose those risks. Sustainability reports varied wildly in scope, depth, and honesty. That created a problem. Investors could not compare risk across portfolios. Greenwashing flourished. And accountability, too often, became optional.

That era is ending. IFRS S2 is fundamentally reshaping how companies identify, manage, and communicate climate-related financial risks and opportunities. For ESG professionals, business leaders, investors, and policymakers, understanding this standard is no longer academic. It is essential.

What Is IFRS S2?

IFRS S2, formally titled Climate-related Disclosures, is a global sustainability reporting standard issued by the International Sustainability Standards Board, commonly known as the ISSB. The ISSB is a body established by the IFRS Foundation, the same organisation responsible for the widely adopted international financial reporting standards used in over 140 countries.

The ISSB published IFRS S2 in June 2023, alongside its companion standard IFRS S1, which addresses general sustainability-related financial disclosures. Together, these two standards form the foundation of a new global baseline for sustainability reporting. While IFRS S1 sets the overarching framework for how companies should disclose material sustainability information, IFRS S2 drills specifically into climate. It focuses on the financial effects of climate-related risks and opportunities across a company’s activities, value chain, and financial planning.

Importantly, IFRS S2 builds on the recommendations of the Task Force on Climate-related Financial Disclosures, or TCFD, which has served as the de facto standard for climate risk disclosure since 2017. By incorporating TCFD into a formal IFRS standard, the ISSB has given climate disclosure the same institutional weight as financial accounting. That is not a small shift. That is a structural transformation in corporate reporting.

IFRS S2 is not simply a reporting checklist. It is a framework that requires companies to think deeply about how climate change shapes their financial future.

Why Climate-Related Disclosure Matters Now

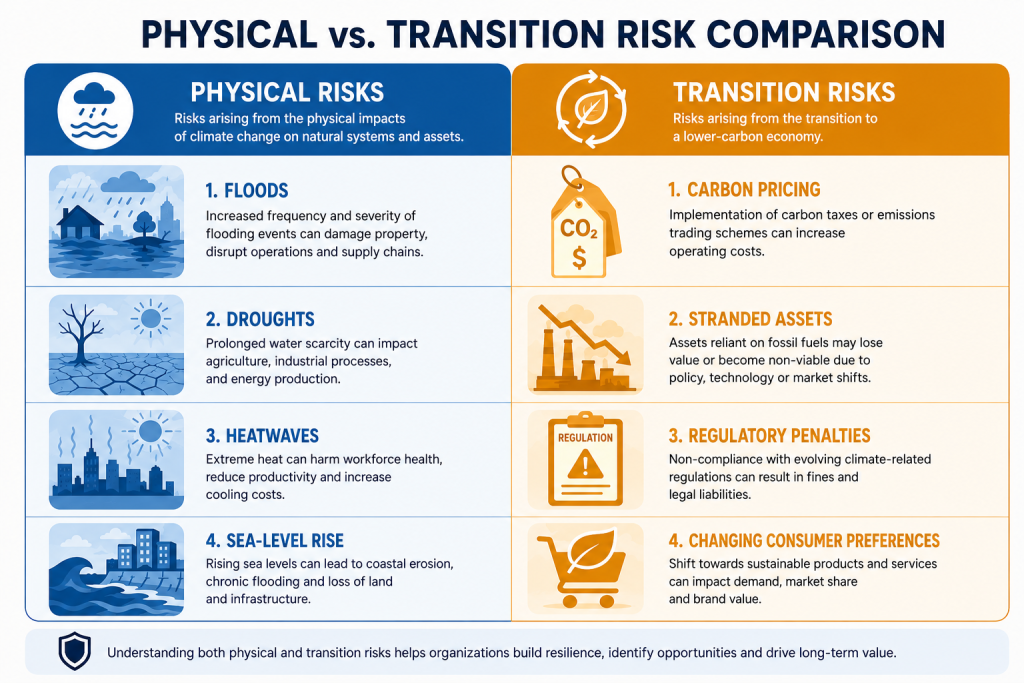

Climate change creates two broad categories of financial risk. Physical risks arise from the direct impacts of a changing climate, including extreme weather events, sea-level rise, and shifting agricultural conditions. Transition risks, on the other hand, emerge from the shift to a lower-carbon economy, through policy changes, technological disruption, and evolving market expectations. Both categories carry real financial consequences, affecting asset values, revenue streams, operating costs, and long-term viability.

Investor expectations have shifted dramatically. Major asset managers, pension funds, and development finance institutions now routinely require climate risk disclosures as part of investment due diligence. Frameworks like the Principles for Responsible Investment, which counts over 5,000 signatories managing more than USD 120 trillion in assets, have embedded climate risk assessment into mainstream investment practice.

Regulatory pressure is also intensifying. The European Union’s Corporate Sustainability Reporting Directive and similar measures in the United Kingdom, Australia, and Japan are all moving toward mandatory climate reporting. IFRS S2 provides an internationally coherent baseline that companies operating across these jurisdictions can use to meet multiple requirements simultaneously.

Furthermore, lenders, credit rating agencies, and insurers are incorporating climate risk into financial assessments. Companies that cannot demonstrate a credible understanding of their climate exposure increasingly face higher borrowing costs, reduced access to capital, and limited insurance coverage. Disclosure, therefore, is no longer a public relations exercise. It is a financial imperative.

The Structure of IFRS S2 Disclosures

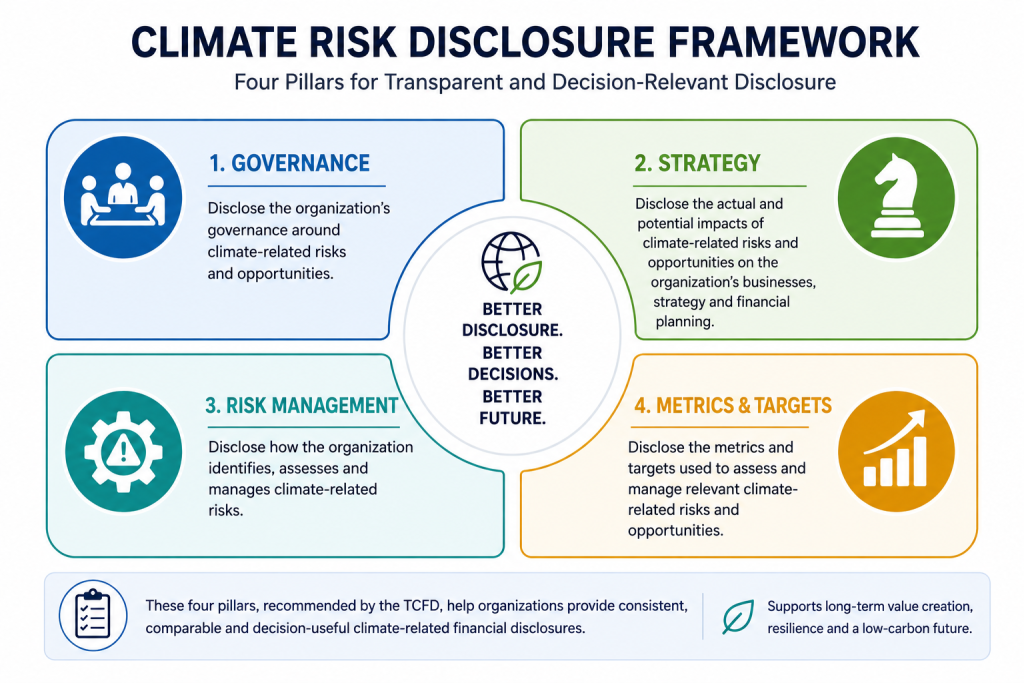

IFRS S2 organises climate-related disclosures around four core pillars, each addressing a different dimension of how a company relates to climate risk and opportunity.

Governance requires companies to disclose how their board and management oversee climate-related risks and opportunities. This pillar asks questions like: Does the board receive regular climate briefings? Who holds accountability for climate strategy? It forces organisations to demonstrate that climate is integrated into their leadership structures, not delegated to a sustainability department in isolation.

Strategy addresses how climate risks and opportunities affect the company’s business model, financial planning, and long-term resilience. Crucially, this pillar requires companies to conduct scenario analysis, testing their strategy against different climate futures, including a scenario aligned with limiting global warming to 1.5 degrees Celsius. This moves climate thinking from narrative to rigorous financial stress testing.

Risk management discloses how a company identifies, assesses, prioritises, and monitors climate-related risks, and how that process integrates into broader enterprise risk management. This pillar connects climate risk to the company’s overall risk governance and operational decision-making.

Metrics and targets require companies to report quantitative information, including greenhouse gas emissions across Scopes 1, 2, and 3, as well as climate-related performance indicators and the targets the company has set. This pillar gives investors and stakeholders the data they need to track progress and compare performance across companies.

IFRS S2 and ESG Reporting Transformation

Before IFRS S2, the sustainability reporting landscape was fragmented. Companies could choose from dozens of frameworks, including GRI, CDP, SASB, TCFD, and many national standards. Each framework had different scopes, methodologies, and requirements. As a result, two companies in the same industry could produce very different disclosures while both technically claiming compliance with established standards.

IFRS S2 changes that by establishing a global baseline. Companies that adopt it provide comparable, consistent, and auditable climate disclosures. For investors managing diversified global portfolios, this comparability is transformative. It means they can meaningfully evaluate climate risk across sectors and geographies using a common framework.

The standard also significantly reduces the conditions under which greenwashing can thrive. Because IFRS S2 requires companies to connect climate disclosures directly to financial impacts, vague claims about sustainability become harder to sustain. A company cannot simply assert that it is committed to net zero without also explaining how that commitment affects its capital allocation, revenue projections, and risk profile.

For the first time, sustainability and financial reporting speak the same language. IFRS S2 ensures that climate risk lives inside the financial statements, not merely alongside them.

Moreover, IFRS S2 aligns sustainability reporting with the cadence and rigour of financial reporting. It expects the same level of discipline, governance, and auditability that investors already expect from quarterly earnings reports. That alignment signals a profound shift: climate information is now decision-useful financial information, not corporate goodwill content.

What IFRS S2 Means for Nigeria and Africa

Africa faces a paradox. The continent contributes less than four percent of global greenhouse gas emissions, yet it bears a disproportionate burden of climate impacts. From the Sahel’s expanding desertification to coastal flooding in Lagos and Accra, from agricultural disruption in East Africa to cyclone damage in Mozambique, African economies and communities absorb climate shocks they did not create.

For businesses operating across the continent, IFRS S2 creates both a challenge and an opportunity. The challenge is readiness. Many African companies, particularly small and medium enterprises, lack the data systems, technical expertise, and reporting infrastructure needed to implement comprehensive climate disclosures. Emissions tracking across complex supply chains, scenario analysis, and governance-level climate integration require capabilities that take time and investment to build.

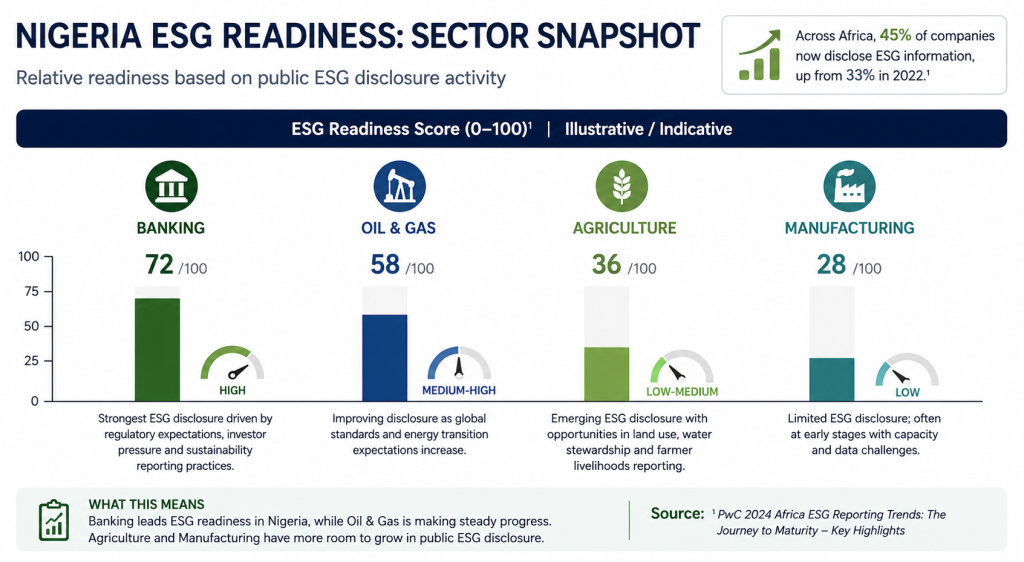

In Nigeria specifically, the Securities and Exchange Commission has been evolving its ESG disclosure requirements, and major banks participating in the Nigerian Sustainable Banking Principles are already engaging with climate risk frameworks. However, the gap between leading institutions and the broader corporate ecosystem remains significant. Capacity building, regulatory clarity, and technical assistance will be essential for Nigerian companies to adopt IFRS S2 meaningfully.

Nevertheless, early adoption carries real advantages. African companies that build credible climate disclosure capabilities early will find themselves better positioned to attract international capital, access green finance instruments, and participate in global value chains where climate standards are increasingly mandatory. The development finance institutions and impact investors that are channelling significant capital into African markets are already using IFRS S2-aligned criteria in their due diligence.

Challenges in Implementing IFRS S2

Recognising the significance of IFRS S2 is one thing. Implementing it is another. Several practical challenges stand between companies and credible compliance.

Data collection and measurement remain the most immediate obstacles. Scope 3 emissions, which cover the indirect emissions across a company’s value chain, are notoriously difficult to measure. For many companies in emerging markets, upstream suppliers and downstream customers do not track or share emissions data consistently. Without accurate data, disclosures become estimates layered on assumptions, which undermines their reliability.

The cost of compliance is also substantial. Building the internal systems, hiring the expertise, and securing the third-party assurance needed for credible IFRS S2 disclosures requires significant investment. For large multinationals, this may be manageable. For mid-sized companies in developing markets, the cost burden can be prohibitive without external support or phased implementation pathways.

Climate expertise is in short supply. Many company boards and executive teams still lack the technical knowledge needed to provide meaningful governance oversight of climate risk. Without informed governance, the governance pillar of IFRS S2 risks becoming a compliance exercise rather than a genuine reflection of strategic oversight.

Finally, inconsistent implementation remains a risk. Because IFRS S2 provides principles-based guidance rather than prescriptive rules in some areas, companies may interpret requirements differently, potentially recreating the comparability problems the standard was designed to solve. Robust assurance standards and regulatory enforcement will be necessary to ensure the standard achieves its intended purpose.

Can IFRS S2 Drive Real Climate Action?

This is the most important question. Disclosure standards can measure and reveal. However, they cannot, by themselves, decarbonise an economy. So does IFRS S2 actually drive behaviour change, or does it simply produce better-formatted inaction?

The evidence from financial markets suggests that disclosure does influence corporate behaviour, particularly when investor pressure follows. When companies must publicly quantify their Scope 1, 2, and 3 emissions and connect those figures to their financial outlook, the risk of climate exposure becomes harder to ignore internally. Management teams that previously treated climate as a communications challenge start treating it as a financial planning variable.

Investor activism, moreover, has grown significantly more sophisticated. Shareholders are filing climate resolutions, voting against directors who fail to demonstrate climate oversight, and divesting from companies that cannot show a credible transition pathway. IFRS S2-aligned disclosures give these investors the specific, comparable data they need to act with precision rather than gesture.

Disclosure is not the destination. However, in a world where what gets measured gets managed, IFRS S2 is a powerful accelerant of the journey toward genuine climate accountability.

Still, honest advocates of the standard acknowledge its limits. IFRS S2 does not mandate emissions reductions. It does not price carbon. It does not change the underlying economics that make fossil fuel investments attractive in certain markets. What it does is remove the information asymmetry that has allowed companies to obscure climate risk and delay meaningful action.

Combined with supportive regulation, credible carbon markets, green finance incentives, and genuine political will, IFRS S2 becomes one critical component of a larger architecture for climate accountability. Alone, it is insufficient. As part of a coherent policy ecosystem, it is indispensable.

For corporate leaders reading this in Lagos, Nairobi, Johannesburg, or Accra, the practical takeaway is clear. IFRS S2 is here to stay. The companies that begin building their climate data systems, strengthening board-level climate literacy, and integrating climate risk into their strategic planning now will be better prepared for the regulatory, investor, and market expectations that are already taking shape. Those that wait face the risk of being caught flat-footed, not by environmental activists, but by their own financiers.

Climate change is not waiting. Neither should the businesses that must navigate it.

[give_form id="20698"]